Many of us make efforts to leverage the latest technology but keeping up does not go without its challenges. In this year of Covid-19, we have been forced to dive into aggressively utilizing technology out of necessity without “doing our homework” as thoroughly as we might have in different circumstances. School districts are motivated to move away from cash transactions for two reasons.

Overall, moving to inbound electronic payment transactions in replacement of cash or high levels of accounts receivable has several benefits.

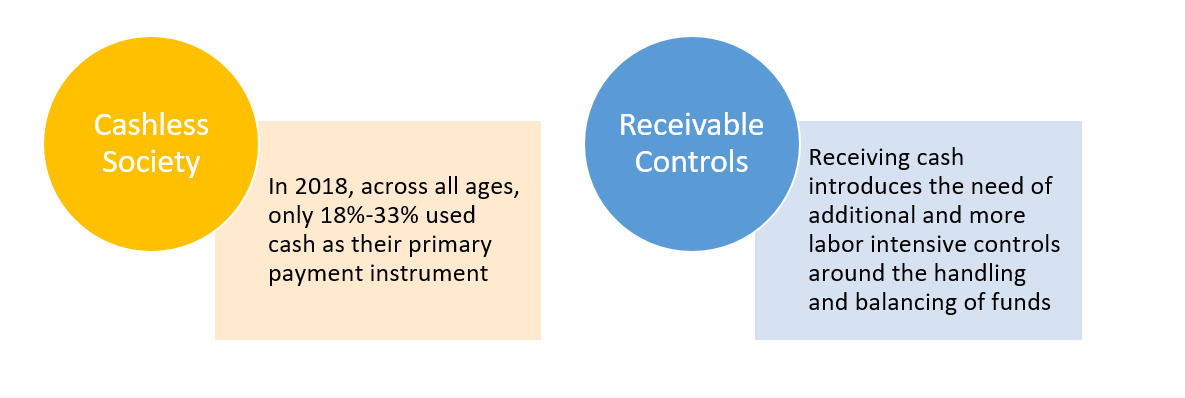

- Near-elimination of “opportunity” for accounts receivable embezzlement

- Less cash-on-hand, therefore decreasing visits to bank deposit box

- Electronic tracking decreasing manual errors, counting, and tracing challenges

- Less dependence on manual, labor intensive processes that require highly trusted individuals

Our intent is to provide a level of pre-work so that organizations can quickly and comfortably evaluate and decide if you want to pursue the use of the latest money transfer technology. This article will not include the scope of online school payment solutions which focus on having accounts to be established in relation to a student. Instead, the focus is on the ad-hoc payment from anyone in the public for things such as tickets to sporting events and the purchase of spirit wear.

We are going to dig in and provide comparisons to a few of the most common inbound money transfer tools that include PayPal, Venmo, Cash App (formerly Square Cash) and Zelle. Although credit cards are another means to receive payments, we are not going to address them here as most of our intended audience is familiar with the pros and cons of accepting credit card payments. Key items and concerns that naturally come to mind when deciding on a money transfer tool are cost, effort to implement/train, fraud protection, accountability, controllability, and security.

We first want to outline a quick and high-level view of the Pros and Cons of these capabilities. This is intended to help you establish an initial determination of which tool(s) might best fit your specific organizational needs as the objectives and implementation vary.

Overall, the differentiating features to point out may assist you in selecting the “best fit” payment transaction tool for your organization:

Instant transfer of money – When utilizing these tools for immediate services (gate fees, donations), it is prudent to utilize a tool that instantly deposits the money. If a payer can dispute or cancel the payment, you will have effort to track and find who and why they cancelled their payment.

Reporting – Access to data/reporting will allow organizations to establish accountability and auditability. Be sure the reporting meets your needs.

Refunding or Disputes – This feature could beneficial, however there are other means of refunding if required.

Ease-of-use - Some software options have significant limitations such as a seller being required to have a specific financial institution account.

Fees – Typically the riskier the transaction, the higher the fees. This could come at a significant expense for those that wish to decrease liability and risk. If the payment company guarantees your funds are available, you will typically pay high fees for that guarantee.

Protections – FDIC insurance (buyer/seller) and 2-factor authentication (buyer) are means to protect involved parties from fraudulent activities.

It is recommended that you continue to do further checking due to the dynamics of the ever-changing environment, but we wanted to take the opportunity to give you an idea of the tools and features some are considering. Every financial transaction has some level of risk and therefore requires you surround that transaction with appropriate controls. Adding capabilities introduces the need for additional controls but may also remove the need for others. One thing you should strongly consider as you head into this new cashless world: Adding capabilities without replacing/removing old ones is a direct impact on your control infrastructure and the time, effort, and cost to manage risk.

Tom Mitchell is the President and CEO of Bonefish Systems, LLC, an OASBO Benchmark Program Provider.