The short answer: for many Ohio school districts, the state-local partnership is becoming less balanced. State education spending can increase statewide while the formula still assigns a larger share of base-cost responsibility to local taxpayers.

Between FY 2022 and FY 2027, the average state-share percentage in the statewide district data declined from 46.5% to 35.2%. The formula-assumed local share moved the other direction, from 53.5% to 64.8%.

That does not automatically mean every district needs more taxes. It does mean taxpayers should ask whether the funding formula is assuming more local capacity than the community can practically convert into recurring revenue.

A roomful of districts tells the story

At a recent in-person seminar with school district finance officials, I asked a simple question: how many of you are forecasting a state-share trend toward Ohio's 10% minimum?

About 17 of the 25 participants raised their hands, representing 17 different school districts.

Then I asked the group to look around the room. Did it seem likely that this many districts in one ordinary training session were truly "minimum state-share" districts in the way most taxpayers would understand that phrase - meaning districts with exceptionally high local capacity, arguably well above average?

The answer in the room was a clear no.

That show of hands was not a scientific survey, but it was an important practitioner reality check. It personalized what the statewide data suggests: the movement toward lower state-share percentages is not limited to a small set of obviously high-capacity communities. Many districts that would not intuitively appear to be near the minimum state-share floor are seeing the formula move in that direction.

For taxpayers, that matters. When a district's state-share percentage trends downward, the formula is not simply reporting a number. It is assigning more of the assumed cost of education to the local community. The question then becomes whether the local tax base can realistically keep pace with that assumption.

The FY 2027 distribution shows the local shift

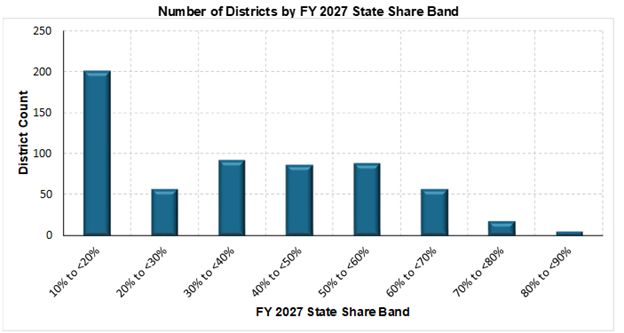

The chart below groups districts by FY 2027 state-share percentage. The distribution is not centered around a 50-50 state-local responsibility split. It is concentrated below 50%.

Figure 1. Districts grouped by FY 2027 state-share percentage. A lower state-share percentage means a higher formula-assumed local share of base cost.

Why the 50% amount matters

The 50% line is not a legal threshold, and Ohio’s formula is not designed to place half of districts above 50% and half below 50%. But it is a useful taxpayer reference point.

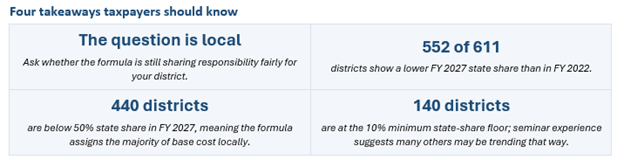

Above 50%, the state is assigned the larger share of base cost. Below 50%, the local community is assigned the larger share. In the FY 2027 data, 440 of 611 districts, about 72%, are below 50% state share.

That does not prove the formula is wrong. It does show that for nearly three out of four districts in the data, the formula is assigning majority responsibility to local resources.

Why the 10% minimum is also important

Ohio’s formula includes a 10% minimum state-share percentage. That floor matters because it applies when the local-capacity calculation would otherwise drive the state share below 10%.

So, when a district is at or near the 10% floor, the formula is effectively treating that district’s local-capacity amount as covering roughly 90% or more of base cost. That does not mean the district has no financial pressure. It means the formula assumes the local community can carry most of the base-cost responsibility.

What this means for levy conversations

This is why taxpayers may hear that Ohio is investing more in schools while local districts still discuss levies, service reductions, or tighter budgets. Both can be true. State spending can rise overall while the formula lowers a district’s state-share percentage.

That can be confusing — and frustrating — for taxpayers and district leaders alike. A levy discussion should not focus only on whether the district is asking for more money. It should also ask whether the state formula has shifted more of the base-cost responsibility to the local side.

Better questions for taxpayers to ask

• What is our district’s FY 2027 state-share percentage?

• Is our district below 50% state share, meaning the formula assigns the majority of base cost locally?

• Is our district at or near the 10% minimum state-share floor?

• Does actual local revenue growth keep pace with the formula’s local-capacity assumption?

• If not, what services, staffing, or programs are at risk?

Bottom line: The local question is not only whether Ohio spends more on schools statewide. The better question is whether the formula is still sharing responsibility fairly for our district, or whether more of that responsibility is shifting to local taxpayers.

Sources: Ohio Revised Code Section 3317.017 (FY 2026 and FY 2027); Ohio Department of Education and Workforce, Overview of School Funding. District counts are based on FY 2022 and FY 2027 state-share data for 611 Ohio school districts provided for analysis.